Eli Lilly and Company

Analysis Result: 4 out of 5 MUMAKS

Rating

This analysis evaluates Eli Lilly and Company according to the UMBRELLA strategy using the MUMAK method. The evaluation is carried out along five decision phases: Geopolitics, Industry, Fundamentals, Market Sentiment, and Technical Analysis.

The goal is not to predict the future precisely. The goal is orientation. We contextualize facts, demonstrate causal relationships, and structure a comprehensible decision logic.

We explain – you decide.

Geopolitics

Classification

The geopolitical and demographic environment remains attractive for Eli Lilly in the long term. Aging populations, the globally increasing number of chronic diseases, and the growing focus on prevention and modern medicines support the demand for innovative therapies. Simultaneously, national pharmaceutical production, supply security, and investments in the healthcare sector continue to gain importance worldwide.

Key Takeaway

- The aging global population increases the demand for therapies for chronic diseases.

- Obesity and diabetes are among the biggest challenges in healthcare worldwide.

- Governments promote medical innovations but simultaneously increase pressure on drug prices.

- Healthcare in the US and Europe is increasingly focusing on effective and long-term cost-efficient therapies.

- Production capacities are becoming a decisive competitive advantage, especially in the GLP-1 market.

MUMAK.me Assessment Phase 1: Positive = 1 MUMAK

Eli Lilly and Company

Geopolitics Rating: positive

Industry

Assessment

Eli Lilly operates in one of the most attractive growth segments of the global healthcare market. The market for GLP-1 therapies for the treatment of obesity and diabetes continues to grow dynamically, supported by high patient demand, increasing medical need, and additional application possibilities. With Mounjaro and Zepbound, Eli Lilly is one of the leading companies in this market and also has a broadly diversified pipeline in oncology, immunology, and neuroscience.

Key Takeaway

- Global demand for obesity and diabetes therapies continues to grow significantly.

- Mounjaro and Zepbound strengthen Eli Lilly’s market leadership in the GLP-1 segment.

- High barriers to market entry arise from long-term clinical development, regulatory requirements, and extensive production capacities.

- Additional growth opportunities arise from oral obesity therapies and innovative drugs in oncology, immunology, and neuroscience.

- Competition with Novo Nordisk and potential new market entrants remains a key factor.

Valuation Comparison: Eli Lilly vs. Pharmaceutical Industry

| Metric | Eli Lilly | Industry average* | Rating |

|---|---|---|---|

| P/E ratio (P/E) | approx. 55–60x | approx. 18–25x | Significant premium |

| EV/EBITDA | approx. 40–45x | approx. 14–18x | Significant premium |

| Dividend Yield | approx. 0.6% | approx. 2–3% | Below average |

| Market Capitalization | approx. USD 1 trillion | Global Large Caps | Globally leading |

*Comparison with major international pharmaceutical companies such as Novo Nordisk, Johnson & Johnson, Merck, Roche, AstraZeneca, AbbVie and Novartis.

MUMAK.me Phase 2 Rating: neutral = 0 MUMAK

Eli Lilly and Company

Industry Rating: neutral

Fundamentals

Assessment

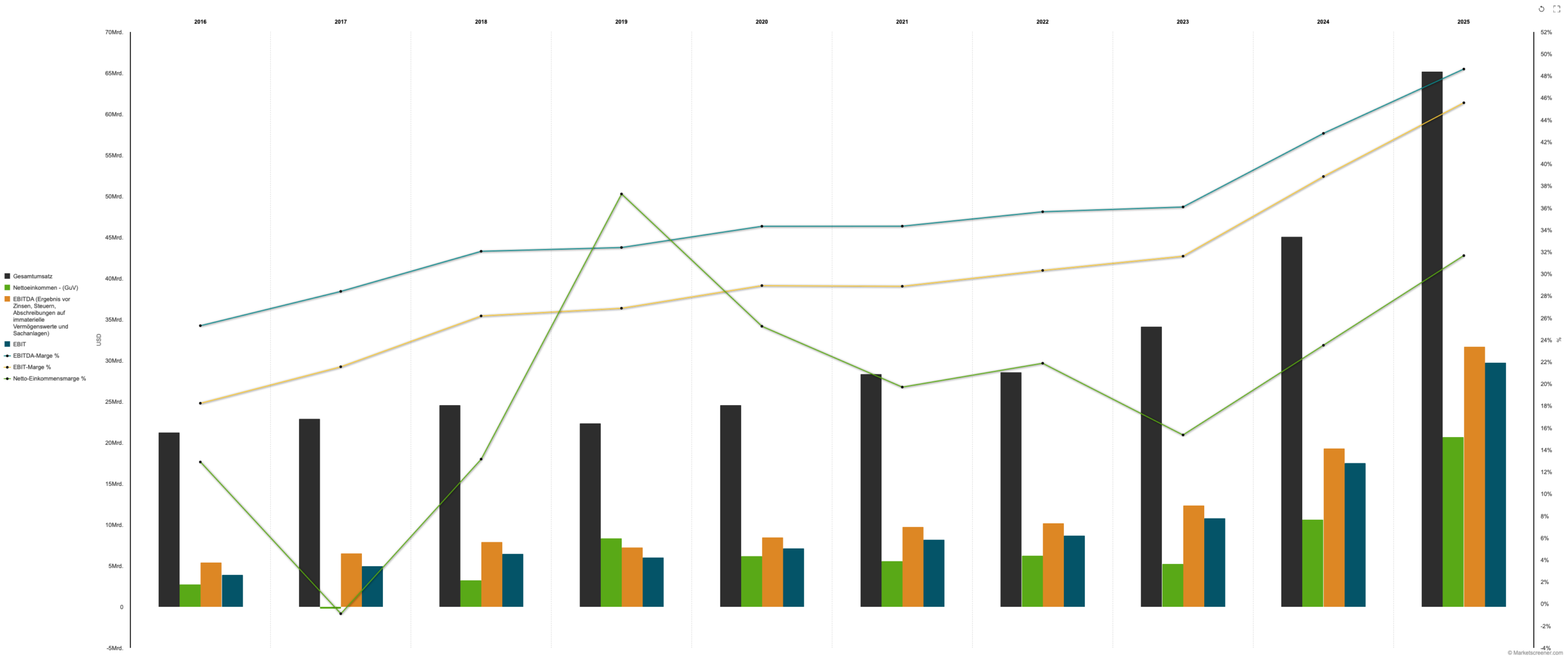

Eli Lilly combines exceptionally strong revenue growth with increasing profitability and continuously rising earning power. The main growth drivers remain Mounjaro and Zepbound, while the rest of the product portfolio further diversifies the company across oncology, immunology, and neuroscience.

Financial Metrics

| Key Figure | FY2024 | FY2025 | FY2026e |

|---|---|---|---|

| Revenue | approx. USD 45.0 billion | approx. USD 65.2 billion | approx. USD 82–85 billion |

| Revenue Growth | approx. 32% | approx. 45% | approx. 26–30% |

| EBITDA | approx. USD 16.1 billion | approx. USD 29.3 billion | approx. USD 37–39 billion |

| EBITDA Margin | approx. 36% | approx. 45% | approx. 45–46% |

| Net Profit | approx. USD 10.6 billion | approx. USD 20.6 billion | approx. USD 31–33 billion |

| Diluted EPS | approx. USD 12.99 | approx. USD 22.95 | approx. USD 35.50–37.00 non-GAAP |

| Free Cash Flow | approx. USD 3.8 billion | approx. USD 9.0 billion | increasing significantly |

| Net Debt / EBITDA | approx. 1.9x | approx. 1.2x | below 1.0x possible |

| Dividend Yield | approx. 0.6% | approx. 0.6% | low, but growing |

Eli Lilly reported revenue growth of 56% to $19.8 billion in Q1 2026 and raised its full-year 2026 revenue guidance to $82–85 billion. The non-GAAP EPS forecast is $35.50–37.00.

Key Takeaway

- Revenue growth remains exceptionally strong.

- Mounjaro and Zepbound are the main growth drivers.

- Profitability improves through economies of scale and patent-protected premium drugs.

- Free cash flow increases significantly despite high investments in production capacities.

- Debt remains well under control.

- Dividend growth continues, but the stock is not a classic dividend stock.

MUMAK.me Assessment Phase 3: Positive = 1 MUMAK

Eli Lilly and Company

Fundamentals Rating: positive

News, Analysts, and Market Sentiment

Assessment

Market sentiment towards Eli Lilly remains very positive. The persistently high demand for GLP-1 therapies, the again raised forecast, and analysts’ confidence in long-term growth support the investment case. At the same time, expectations for the company are now very high, meaning even minor disappointments in prescription numbers, price development, or production capacities can lead to increased volatility.

Key Takeaway

- The Q1 2026 results confirmed the continued very strong demand for Mounjaro and Zepbound.

- Management raised its revenue and earnings guidance for the full year 2026.

- Analysts remain largely optimistic and expect further growth in the obesity and diabetes therapy market.

- Eli Lilly continues to invest billions in expanding its global production capacities.

- Progress in the development of oral GLP-1 medications could represent an important additional growth driver.

Analyst Assessment

| Number of Analysts | ~USD 99 |

| Average Price Target | ~1,220 USD |

| Upside to Average Target | +1,8 % |

| Upper Target | 1,500 USD |

| Lower Target | 850 USD |

Source: MarketScreener, as of July 2026.

Interesting Fact

Within just a few years, Eli Lilly has evolved into one of the world’s most valuable healthcare companies. The key driver behind this is the transformation of obesity treatments from a niche indication into one of the largest structural growth markets in the global pharmaceutical industry.

Mounjaro and Zepbound are no longer viewed exclusively as medications for diabetes or obesity, but as central therapies for the entire field of metabolic health. This market potential could expand significantly further in the coming years through additional indications.

MUMAK.me Evaluation Phase 4: Positive = 1 MUMAK

Eli Lilly and Company

Market Sentiment Rating: positive

Technical Analysis

Assessment

Eli Lilly’s technical structure has improved significantly again in recent months. After the correction down to the area of $850, a dynamic recovery move emerged, bringing the price back to the previous all-time high around $1,230. The stock is currently consolidating just below this resistance at an elevated level.

Key Takeaway

- The long-term uptrend remains intact.

- The stock is consolidating just below its all-time high.

- A breakout above $1,230 would deliver a new technical buy signal.

Development in recent weeks/months

As of: July 1, 2026

RSI (14)

Neutral to slightly positive

- Current RSI: approx. 62

- No Overbought Condition

- Momentum remains positive

Interpretation: The RSI signals an intact uptrend. Despite the strong rally, there is currently no extreme overheating.

MACD (12/26/9)

Slightly positive

- MACD is trading above the zero line

- Positive trend structure remains intact

- Short-term slight weakening of momentum after the strong upward move

Interpretation: The overarching uptrend remains intact. After the rally, the MACD is currently in a normal consolidation phase.

Bollinger Bands (20)

Neutral to slightly bullish

- Price is trading in the upper range of the Bollinger Bands

- Pullback occurred within the band

- Bands remain open and reflect the strong trend

Interpretation: The current movement points more toward consolidation within an existing uptrend rather than a trend reversal.

Conclusion

Eli Lilly continues to present a technically strong position. After the dynamic recovery since the April low, the stock is consolidating just below its all-time high. RSI and MACD confirm the overarching uptrend without signaling pronounced overheating. A sustained breakout above $1,230 would significantly increase the probability of a continuation of the long-term uptrend. Overall, the technical outlook remains positive to slightly bullish.

→ MUMAK.me Rating Phase 5: Positive = 1 MUMAK

Eli Lilly and Company

Technical Analysis Rating: positive

Summary

Eli Lilly is currently one of the most attractive growth companies in the global healthcare sector. The company benefits from its leading position in the rapidly growing GLP-1 market, exceptionally strong revenue and earnings development, and a broadly diversified innovation pipeline in oncology, immunology, and neuroscience.

The biggest challenge remains the demanding valuation. A significant portion of the expected future growth is already priced into the stock. To justify this valuation in the long term, Eli Lilly must maintain its high growth rate, further expand production capacities, and successfully translate its pipeline into new products.

From a long-term perspective, however, Eli Lilly remains one of the highest-quality companies in the global pharmaceutical industry and is likely to remain one of the most important innovation drivers in the healthcare sector in the coming years.

Rating According to the MUMAK Method

| Category | Rating |

|---|---|

| Geopolitics | Positive |

| Industry | Neutral |

| Fundamentals | Positive |

| News & Sentiment | Positive |

| Technical Analysis | Positive |