Leonardo S.p.A.

Analysis Result: 4 out of 5 MUMAKS

Rating

This analysis evaluates Leonardo S.p.A. according to the UMBRELLA strategy using the MUMAK method. The evaluation is carried out across five decision phases: Geopolitics, Industry, Fundamentals, Market Sentiment, and Technical Analysis.

The goal is not to predict the future precisely. The goal is orientation. We contextualize facts, demonstrate causal relationships, and structure a comprehensible decision logic.

We explain – you decide.

Geopolitics

Classification

The current geopolitical environment remains highly supportive for European defense and aerospace companies.

Key Takeaway

- European defense spending continues to rise, supported by NATO spending targets.

- The war in Ukraine, instability in the Middle East, and Europe’s desire for greater strategic autonomy continue to drive demand for air defense, electronics, helicopters, aircraft, cyber, and space technologies.

- NATO reported that European allies and Canada increased their defense spending by 20% in 2025 compared to 2024.

- Leonardo is strategically positioned as one of Europe’s leading defense providers with a strong presence in Italy, Europe, NATO programs, and selected international markets.

- Nevertheless, in a recent report, Morgan Stanley downgraded the European defense sector to “neutral.”

MUMAK.me Assessment Phase 1: Positive = 1 MUMAK

Leonardo S.p.A.

Geopolitics Rating: positive

Industry

Assessment

The defense and aerospace industry continues to benefit from structural demand growth, multi-year procurement cycles, and high visibility in order intake.

Key Takeaway

- Higher European defense spending supports demand for platforms, electronics, sensors, secure communications, helicopters, and training systems.

- Long-term programs such as Eurofighter, GCAP, MBDA, space systems, and helicopter fleets create planning certainty over multiple years.

- Leonardo’s order backlog exceeded EUR 46 billion at the end of fiscal year 2025 and rose to EUR 57 billion in the first quarter of 2026 following the consolidation of Iveco Defence Vehicles.

- The acquisition of Iveco Defence Vehicles strengthens Leonardo’s position in land systems and expands the portfolio to include wheeled and tracked vehicles for military applications.

- The average large defense and aerospace company is currently valued at approximately a P/E ratio of 22–25 and an EV/EBITDA of 12–14. Leonardo, with a P/E of 22.1 and an EV/EBITDA of 11.4, is slightly below this industry average and thus appears rather attractively valued despite its strong market position.

MUMAK.me Assessment Phase 2: Positive = 1 MUMAK

Leonardo S.p.A.

Industry Rating: positive

Fundamentals

Assessment

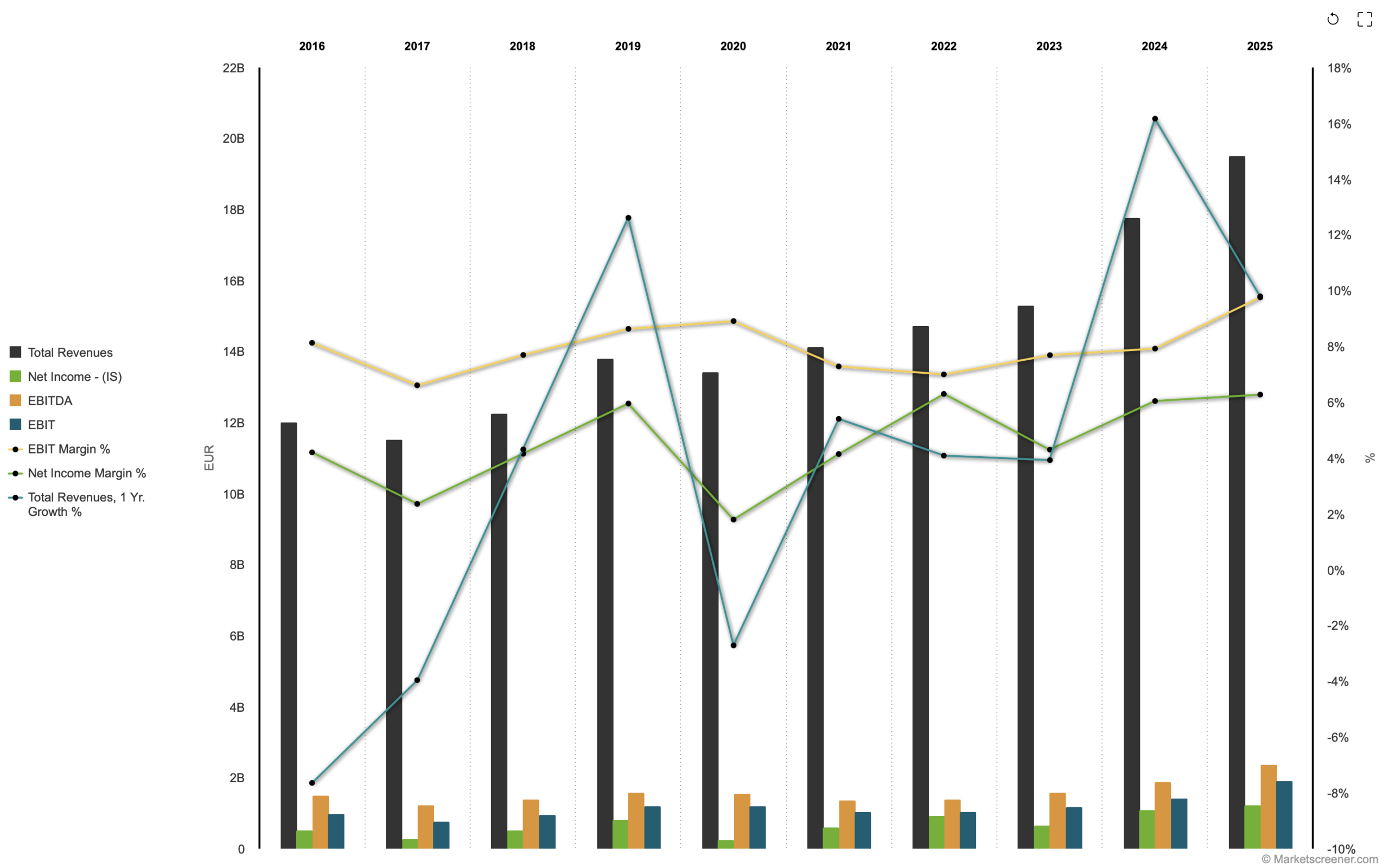

Leonardo achieved strong growth in fiscal year 2025 and confirmed an improved financial outlook for 2026 with rising profitability, higher cash flow generation, and growing order intake.

Key Takeaway

- Strong growth continues in 2026. Leonardo expects revenue to increase to approximately EUR 21.0 billion, after revenue already rose by 11% to EUR 19.5 billion in 2025.

- Record order intake supports future growth. New orders reached EUR 23.8 billion in 2025, 15% above the prior year.

- Profitability is improving faster than revenue. EBITA rose by 18% to EUR 1.75 billion in 2025, growing more strongly than revenue. Management expects a further increase in 2026.

- Rising defense spending remains a key growth driver. Higher budgets in Europe and within NATO, as well as strong demand for aerospace, defense, and security systems, support the company’s positive development.

Outlook 2026

| Key Figure | FY 2025 / 2026e |

|---|---|

| Revenue | ~ EUR 21.0 billion |

| EBITA | ~ EUR 2.03 billion |

| Free Operating Cash Flow | ~ EUR 1.11 billion |

| Group Net Debt | ~ EUR 0.8 billion, excluding cash outflow for IDV acquisition |

| Forward P/E (2026e) | ~ 22x |

Financial Metrics

| Key Figure | FY 2025 |

|---|---|

| Order Intake FY2025 | EUR 23.8 billion (+15% vs. 2024) |

| Revenue FY2025 | EUR 19.5 billion (+11% vs. 2024) |

| EBITA FY2025 | EUR 1.75 billion (+18% vs. 2024) |

| FOCF FY2025 | EUR 1.0 billion (+21% vs. 2024) |

Leonardo S.p.A. – Financial Overview. Source: Leonardo FY2025 Results and Outlook 2026, MarketScreener valuation data, retrieved in June 2026.

→ MUMAK.me Rating Phase 3: positive = 1 MUMAK

Leonardo S.p.A.

Fundamentals Rating: positive

News, Analysts, and Market Sentiment

Assessment

Market sentiment remains constructive, supported by high demand in the defense sector, a large order backlog, rising profitability, and positive analyst assessments.

Key Takeaway

- Leonardo confirmed its full-year guidance following first-quarter 2026 results. In the first quarter, orders worth EUR 9.0 billion and revenues of EUR 4.4 billion were achieved.

- Analysts remain predominantly positive and see price targets above the current share price.

Analyst Consensus

| Average Recommendation | OUTPERFORM |

| Number of Analysts | 18 |

| Average Price Target | ~EUR 68.67 |

| Upside to Average Target | approx. +32% |

| Upper Target | ~EUR 83.00 |

| Lower Target | ~EUR 62.00 |

Source: MarketScreener, retrieved in June 2026.

Interesting Fact

Leonardo completed the acquisition of Iveco Defence Vehicles in March 2026. This expanded the existing portfolio of electronics and system solutions to include land systems and further strengthened its position as a fully integrated defense company.

MUMAK.me Evaluation Phase 4: Positive = 1 MUMAK

Leonardo S.p.A.

Market Sentiment Rating: positive

Technical Analysis

Assessment

The technical structure remains positive in the medium term, even though the stock is currently undergoing a consolidation phase within a still-intact uptrend following the 2026 highs.

Key Takeaway

- The stock continues to trade well above prior-year levels and reflects the strong revaluation of European defense companies.

- Short-term momentum is mixed: The stock is up year-to-date but trading below its annual high, suggesting consolidation after the strong rally.

- A breakout above recent highs would confirm renewed upward momentum, while a decline below the current trading range would cloud the technical picture.

Performance over the past weeks/months (As of 1106/2026)

RSI (14)

Neutral to slightly positive

- Current RSI: approx. 51

- No overbought or oversold condition

Interpretation: Neutral with a slightly positive bias.

MACD (12/26/9)

Early buy signal

- MACD slightly positive

- Negative trend of recent weeks losing momentum

Interpretation: Possible early signs of trend improvement following consolidation.

Bollinger Bands (20)

Neutral to slightly bullish

- Price trading above the middle Bollinger Band

- Bollinger Bands beginning to widen slightly again

Interpretation: Consolidation appears largely processed; potential for a new upward move is increasing.

The overall indicator interpretation is neutral.

MUMAK.me Rating Phase 5: Neutral = 0 MUMAK

Leonardo S.p.A.

Technical analysis rating: neutral

Summary

The analysis shows an overall stable positive picture with an attractive long-term strategic positioning.

→ Geopolitics → Industry → Fundamental Data → Market Sentiment → Chart Analysis

Leonardo benefits from a highly supportive European defense cycle, strong operational performance in fiscal year 2025, a growing order backlog, rising profitability, and positive market sentiment.

The investment thesis continues to be supported by geopolitical factors, industry demand, and strong fundamentals. Key risks include valuation, operational execution, supply chain issues, and the timing of government procurement programs.

Rating According to the MUMAK Method

| Category | Rating |

|---|---|

| Geopolitics | Positive |

| Industry | Positive |

| Fundamentals | Positive |

| News & Sentiment | Positive |

| Technical Analysis | Neutral |