Brief Introduction – Equinor

The global energy market continues to be shaped by geopolitical tensions, supply shortages, and structurally robust demand. The importance of natural gas, in particular, has significantly increased, especially in Europe, where energy supply security has become a strategic priority.

In this environment, companies with high gas exposure and access to stable production regions benefit not only from price developments but also from their geopolitical positioning.

Equinor is one of the key players in this context. The Norwegian energy company combines oil and gas production with a strong focus on European energy supply and growing investments in renewable energies.

30.04.2026

This analysis structures the investment decision along five categories: Geopolitics, Industry, Fundamentals, Market Sentiment, and Technical Analysis.

The goal is not to predict the future precisely. The goal is orientation. We contextualize facts, demonstrate causal relationships, and structure a comprehensible decision logic.

We explain – you decide.

Equinor

Analysis Result: 5 out of 5 MUMAKS

Rating

Geopolitics

Assessment

Geopolitics is a direct driver for oil and gas prices and a particularly important factor for European gas supply. For Equinor, this dimension plays a larger role than for many competitors, as the company combines upstream exposure with a strategically important role in Europe’s gas supply.

Key Takeaway

Equinor directly benefits from geopolitical tensions due to its strong gas exposure and its role as a central supplier to Europe, while Norway’s stable political environment reduces geopolitical downside risks.

Rationale

Energy security in Europe as a structural driver

As Europe increasingly focuses on a secure gas supply, Norwegian gas has gained strategic importance.

Stable Production Region

In contrast to producers with stronger exposure to politically unstable regions, Equinor’s Norwegian Continental Shelf production offers a significantly more stable geopolitical environment.

Direct Lever on Gas and Oil Prices

Equinor is not only an oil producer but also a significant gas supplier.

Conclusion

Geopolitical tensions and Europe’s focus on energy supply security strengthen Equinor’s strategic relevance and support its earnings profile.

Equinor

Geopolitics Rating: positive

Industry

Assessment

The integrated energy sector remains cyclical, but is currently characterized by supply discipline, high infrastructural relevance, and a stronger strategic role for gas.

Key Takeaway

Equinor is structurally well-positioned within the industry, supported by a strong gas position, a low-risk asset base in Norway, and an integrated portfolio of oil, gas, trading, and energy.

Rationale

Strong Position in the European Gas Market and Norwegian Offshore Sector

Assets on the Norwegian Continental Shelf remain a key value driver. At the same time, the company aims to maintain production levels from 2020 to 2035.

Integrated Portfolio Reduces Dependence on Individual Segments

Equinor is not just an upstream producer. The Marketing, Midstream, and Processing segment delivered strong results in Q4 2025, supported by gas trading, optimization, and positive price effects.

International Oil and Gas Growth with Disciplined Capital Allocation

Equinor continues to focus on selective international growth in the oil and gas sector while simultaneously building an integrated energy business.

Conclusion

Equinor benefits from a favorable industry position: strong gas relevance, robust offshore production, and a more diversified integrated business model than many pure upstream companies.

Equinor

Industry Rating: positive

Fundamentals

Assessment

Fundamentals show whether Equinor can sustainably convert its strategic position and favorable market standing into earnings, cash flows, and capital returns.

Key Takeaway

Equinor remains cash flow strong and operationally resilient, supported by stable revenues, high profitability, and disciplined capital allocation, despite a normalization of results.

Rationale

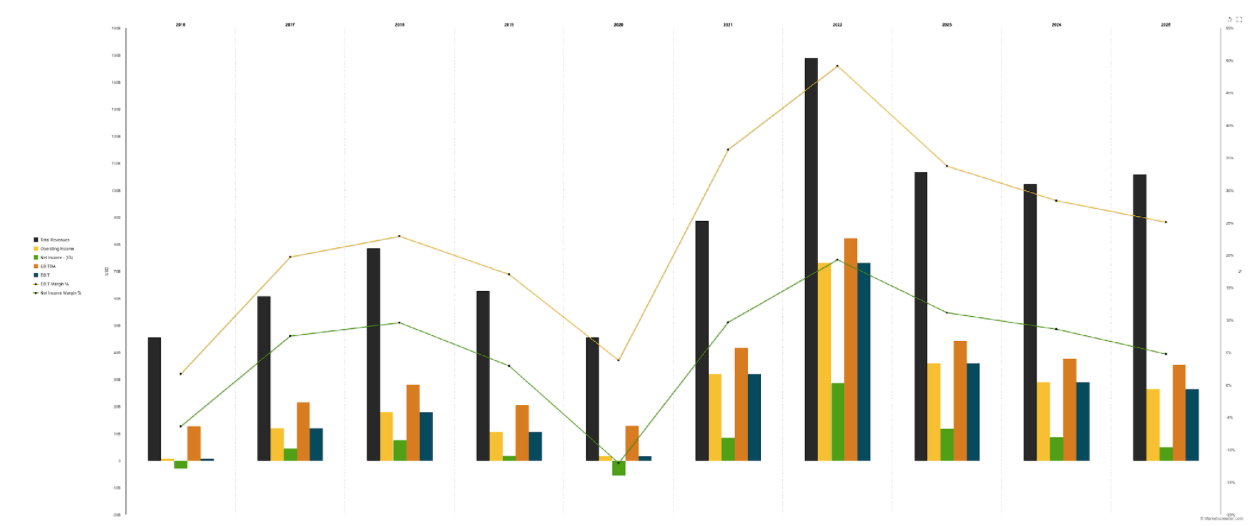

Revenue and Earnings (Fiscal Year 2025)

| Revenue and Earnings (Fiscal Year 2025) | ||

|---|---|---|

| Revenue: | ~$106 billion | (vs. ~$103 billion YoY) |

| Net Income: | ~$5.04 billion | (vs. ~$8.81 billion YoY) |

| Diluted EPS: | ~$1.94 | (vs. $3.11 YoY) |

The development shows:

- stable revenue development, driven by production and gas exposure

- however, declining results due to lower commodity prices and margin normalization

→ Normalization of results after a strong cycle

Margin Development

| Margin Development | |

|---|---|

| EBITDA Margin: | ~16.8% |

| Net Margin: | ~9.5% (vs. ~12.3% YoY) |

Interpretation:

- Margins remain at a structurally solid level

- however, show pressure compared to peak cycles

→ Profitability stabilizes at normalized levels

Rating

| Rating | |

|---|---|

| P/E 2026: | ~10.9 |

| P/E 2027: | ~12.3 |

→ relatively low valuation, reflecting cyclicality

Profitability

| Profitability | Table Header | Table header |

|---|---|---|

| EBITDA: | ~$35.5 billion | |

| EBIT: | ~$25.6 billion |

This highlights:

- high absolute earning power

- strong operational scaling, especially in the gas and offshore sectors

Cash Flow and Capital Discipline

| Cash Flow & Capital Discipline | Table Header |

|---|---|

| Operating Cash Flow: | ~$20 billion |

| Free Cash Flow: | ~$22.6 billion |

This enables:

- high financial flexibility

- continuous capital returns and investments

→ Cash flow remains the central strength of the business model

Dividend and Capital Allocation

| Dividend & Capital Allocation | Table Header |

|---|---|

| Annual Dividend: | ~$1.40–1.50 per share |

| Dividend Yield: | ~6–7% |

Equinor has a high and attractive dividend yield, supported by strong cash flows.

Additionally, the company continues to implement share buybacks as part of its capital return strategy.

→ Focus on high shareholder returns with disciplined reinvestment

Conclusion

Equinor demonstrates strong cash flow generation, solid profitability, and an attractive capital return profile.

The decline in results reflects a cyclical normalization and not a structural weakness.

Equinor

Fundamentals Rating: positive

News, Analysts, and Market Sentiment

Assessment

Market sentiment reflects expectations regarding energy prices, capital allocation, and investment cycles in the energy sector.

Key Takeaway

Sentiment towards Equinor is constructive, supported by stable analyst expectations and the company’s strong position in the European gas market.

Rationale

Analyst Estimates

| Analyst Overview | Table Header |

|---|---|

| Average Price Target | ~$33.91 |

| Upper Range: | $42.81 |

| Lower Range: | $22.07 |

→ Analysts view Equinor as a stable energy player, but consider the cyclical nature of the business

Market Positioning

Equinor is typically classified as:

- Core investment in the European energy sector

- Key player in the gas market

- Dividend-oriented energy stock

Capital Flows

Institutional investors allocate capital to Equinor for:

- Participation in European energy supply security

- Leveraging cash flow-strong commodity exposure

Macro Narrative

- central role of gas in the European energy transition

- continued focus on supply security

- limited short-term alternatives to fossil fuels

Conclusion

Market sentiment remains constructive, but reflects the cyclical and commodity-driven nature of the business.

Equinor

Market Sentiment Rating: positive

Technical Analysis

Assessment

Technical analysis structures the timing framework for a position.

Key Takeaway

Equinor’s technical structure shows a strong uptrend with short-term overextension and beginning consolidation near resistance.

Rationale

Bollinger Bands

The price has moved significantly above the upper Bollinger Band.

This signals:

- strong trend acceleration

- short-term overextension

The subsequent move back into the band indicates a beginning consolidation.

RSI

The RSI is in the range of ~65–70.

This means:

- clear uptrend (above 50)

- approaching overbought zone

→ short-term cooling likely

MACD

The MACD shows strong positive momentum at a high level.

This signals:

- intact trend

- however, initial signs of potential weakening after a strong move

Conclusion

The technical structure confirms a very strong uptrend with a short-term overheating tendency.

Consolidation below resistance is likely before the trend can continue.

Equinor

Technical Analysis Rating: positive

Summary

The analysis shows a consistent and robust overall picture:

Geopolitics → Industry → Fundamentals → Sentiment → Technical Analysis

All five levels deliver a positive signal.

Equinor benefits from the increasing geopolitical importance of energy supply, particularly through its strong position in the European gas market. The company combines stable production from a low-risk region with direct exposure to oil and gas prices.

At the same time, Equinor shows solid fundamentals, strong cash flow generation, and an attractive capital return profile.

Decision Logic

- direct leverage on oil and gas prices, especially in the European gas market

- strong positioning in a geopolitically stable production region

- robust fundamentals with strong cash flow generation and attractive dividend

- constructive sentiment due to energy supply security and stable demand

- intact technical uptrend with short-term consolidation risk

Rating According to the MUMAK Method

| Category | Rating |

|---|---|

| Geopolitics | Positive |

| Industry | Positive |

| Fundamentals | Positive |

| News & Sentiment | Positive |

| Technical Analysis | Positive |